OTTAWA – BUSINESS – The Canadian Real Estate Association (CREA) has updated its forecast for home sales activity via the Multiple Listing Service® (MLS®) Systems of Canadian real estate boards and associations.

Monthly home sales over Canadian MLS® Systems were not as volatile in 2021 as they were in 2020. That said, they were nonetheless still very unstable – similar to what was seen during the 2008-2009 financial crisis – but at a much higher level.

This volatility, ranging from a seasonally adjusted annualized high of 807,250 sales in March 2021 to a low of 585,250 sales in August 2021, then back up to around 650,000 at the time of this writing, was not the result of lockdowns or any major fluctuations in demand.

Rather, with the end-of-month supply of homes for sale setting new record-lows every month this year, it would seem the ups and downs of sales in 2021 had more to do with where and how many properties came up for sale. When they did, the demand was there to scoop them up.

The number of months of inventory has only dipped below 2 months four times in history – in February and March of 2021, and then again in October and November – so it is not surprising that prices nationally rose by more than 20% in 2021 compared to 2020. While price growth is not expected to be as extreme in 2022, many of the conditions that supported it right up until the end of 2021 will still be there on New Year’s Day.

Along with an unprecedented supply crunch, there are quite a few other factors that will play important roles in Canadian housing markets in 2022. Ongoing strong demand from an unobservable but no doubt large number of households waiting for new listings to show up will be one tailwind.

Many of those listings will likely show up as existing owners continue to move around in record numbers in response to the changes to our lives since the emergence of the COVID-19 pandemic. Demand should be further turbocharged by, and buyers will face increased competition from, the return of very strong or perhaps even all-time record levels of international immigration, depending on the evolution of the pandemic.

There will also be headwinds, chief among them higher interest rates. While the Bank of Canada has set the stage for a tightening cycle of still indeterminant size to begin as early as April of next year, mortgage rates have already started to move higher, first this past spring, and again in the last few months.

Those are the rates borrowers are actually getting, but in Canada they must qualify for their mortgage loans at the stress test rate, currently set at 5.25%, which is somewhere in the range of 275-basis points above the typical discounted 5-year rate. While that is less of a spread than earlier this year, it is nonetheless still in “emergency mode”.

At the moment, increases in mortgage rates are only affecting monthly payments, though with a 275-basis point stress test, these are still affordable. It is the level of the stress test, due soon for a re-evaluation by the Office of the Superintendent of Financial Institutions, that governs not what people can afford, but what they are allowed to borrow. As such, this re-assessment is a major wildcard. The fact that it is still quite high means it could be left alone for now to act as a kind of cushion against rising rates for young and/or first-time buyers. After all, the original intent of the policy was a 200-basis point buffer.

And lastly, another wildcard are the promises made around housing in the recent federal election. Which of these will become policy in 2022 and how will they affect housing markets across Canada? Unfortunately, a major increase in new supply (the most needed but also most long-term of all of these interventions) is unlikely to make a major difference within the space of a year.

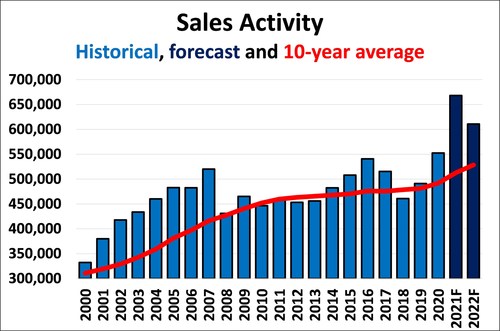

With all of that said, some 668,000 properties are projected to trade hands via Canadian MLS® systems in 2021 — a record-setting number by a margin of about 21% over 2020. This projection is a small upward revision from the September forecast, owing to an unexpected rebound in sales activity in the final quarter of the year.

The national average home price is projected to rise by 21.2% on an annual basis to $687,500 in 2021, again, a little higher than in CREA’s previous forecast. This historically large increase reflects the unprecedented imbalance of housing supply and demand, with the number of months of inventory nationally remaining close to 2 throughout 2021. The long-term average for that measure is more than 5 months.

On a monthly and quarterly basis, sales are forecast to remain historically strong in 2022 while at the same time trending slowly back in the direction of more typical levels. Limited supply, higher prices and higher interest rates are expected to tap the brakes on activity in 2022 compared to 2021; although, increased churn in resale markets resulting from the COVID-19-related shake-up is expected to continue to boost activity above what was normal before COVID-19. Indeed, it is possible that many of the moves associated with changes related to remote work won’t play out until further down the road when we have more certainty about what the future will look like post-COVID-19.

National home sales are forecast to fall by 8.6% to around 610,700 units in 2022 – still the second-best year on record. This easing trend is expected to play out across most of the country with buyers facing both supply and affordability constraints, while at the same time, the urgency to purchase a home base to ride out the pandemic continues to fade.

Still, with supply continuing to hit fresh lows every day, the national average home price is forecast to rise by a further 7.6% on an annual basis to around $739,500 in 2022; although, for context, it should be noted that as of November 2021, the national average price was almost $721,000, making this a somewhat conservative forecast given what the handoff from 2021 to 2022 is looking like.

About the Canadian Real Estate Association

The Canadian Real Estate Association (CREA) is one of Canada’s largest single-industry associations. CREA works on behalf of more than 140,000 REALTORS® who contribute to the economic and social well-being of communities across Canada. Together they advocate for property owners, buyers and sellers.